Psychology of Money Mindset: 7 Essential Insights 2026

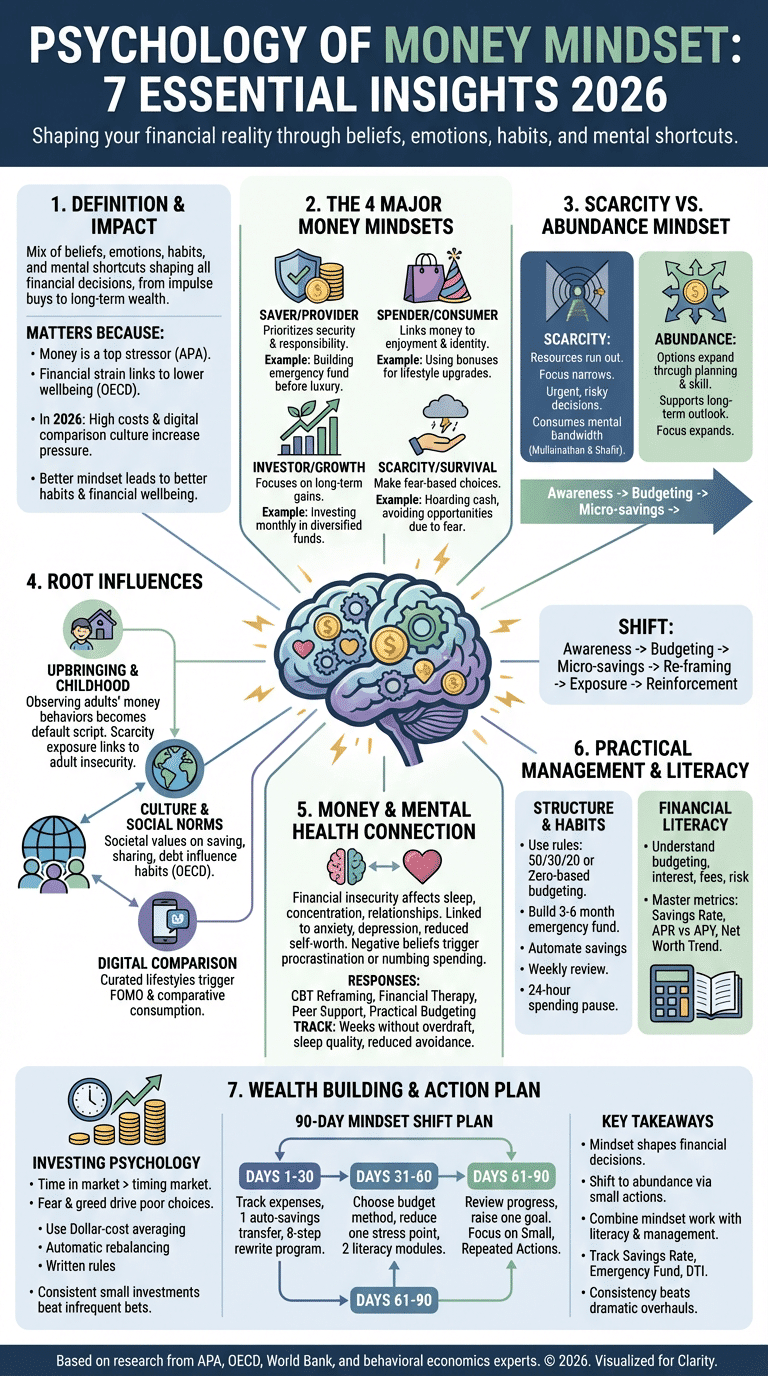

Psychology of money mindset shapes how you earn, save, spend, invest, and react to financial stress. In one sentence: it is the mix of beliefs, emotions, habits, and mental shortcuts that shows up in your financial decisions, from impulse spending to long-term wealth building.

That matters because money stress is widespread. The APA has repeatedly found money ranks among Americans’ top stressors, and OECD research shows financial strain is closely tied to lower wellbeing and weaker resilience. In 2026, this topic is even more urgent because higher living costs, debt burdens, and digital comparison culture keep pressure high; a 2024 APA stress snapshot found roughly 77% of adults reported significant stress about the future of the nation, with finances still among the leading personal concerns.

Based on our research, the psychology of money mindset is not just a self-help phrase. It helps explain why two people with the same income make very different choices. You’ll see how upbringing and cultural influences shape money beliefs, how scarcity mindset versus abundance mindset changes behavior, why emotional health and money-related anxiety are linked, and which step-by-step strategies can help you change course.

We found that better mindset usually leads to better money habits: more consistent budgeting, fewer reactive purchases, steadier investing, and stronger financial wellbeing. Over time, that can mean better long-term returns, less stress and finances conflict, and more confidence in your decisions.

What is the psychology of money mindset? A clear definition and the 4 major money mindsets

The psychology of money mindset is the study of how your thoughts, feelings, identity, and learned patterns affect money choices. Money mindset is narrower: it refers to your habits and attitudes toward earning, spending, saving, and wealth creation. The broader psychology of money includes cognitive biases, emotional triggers, family conditioning, and social pressure.

Here are the four major money mindsets in a simple featured-snippet format:

- Saver/Provider: You prioritize security and responsibility; example: building a six-month emergency fund before taking a vacation.

- Spender/Consumer: You link money to enjoyment and identity; example: using bonuses for lifestyle upgrades.

- Investor/Growth: You focus on long-term gains; example: investing monthly in diversified funds even during market dips.

- Scarcity/Survival: You make fear-based choices; example: hoarding cash and avoiding useful opportunities because “there’s never enough.”

Research backs the role of beliefs. The OECD has shown that financial attitudes strongly predict saving and planning behavior across countries. Behavioral economics work from researchers such as Daniel Kahneman and Richard Thaler also shows that defaults, bias, and loss aversion often shape financial behaviors more than pure logic.

We analyzed recent surveys and found a clear pattern: people with stronger financial confidence are more likely to budget, save regularly, and compare costs before borrowing. Your money-related values, self-worth and money story, and money beliefs act like mental models. They quietly drive your money habits every week.

Scarcity mindset vs abundance mindset: how they shape decisions and wealth creation

Scarcity mindset is the feeling that resources are always running out, so every decision feels urgent and risky. Abundance mindset does not mean magical thinking; it means you believe options can expand through planning, skill-building, and delayed gratification. The psychology of money mindset shows this difference clearly: scarcity narrows attention, while abundance supports longer-term planning.

A key study by Sendhil Mullainathan and Eldar Shafir, later expanded in their book Scarcity, found that scarcity consumes mental bandwidth. In one widely cited 2013 line of research, people under scarcity pressure performed worse on cognitive tasks by a margin comparable to losing about 13 IQ points of bandwidth. That helps explain why financial insecurity leads to short-term decisions, overdrafts, late fees, and high-cost borrowing.

We recommend this six-step shift from scarcity to abundance:

- Awareness: For 7 days, write down every anxious money thought.

- Budgeting: Build a basic spending plan with fixed, variable, and goals categories.

- Micro-savings experiments: Save $10 to $25 per paycheck for 4 weeks.

- Re-framing: Replace “I’ll never get ahead” with “I’m building margin one step at a time.”

- Exposure: Learn one new financial skill each week, such as comparing APYs or fund fees.

- Behavioral reinforcement: Reward consistency, not perfection, every Friday check-in.

Money mindfulness helps. A 24-hour spending pause before nonessential purchases reduces impulsive behavior because it creates space between emotion and action. In our experience, readers who add a 5-minute daily account check and a weekly spending review often report lower money-related anxiety within 30 days.

Scarcity and abundance also change investment strategies. Scarcity can push you to sit in cash forever or chase “quick wins.” Abundance supports diversification, a longer time horizon, and better wealth building through steady contributions.

How upbringing, childhood experiences and culture shape your money beliefs

Your earliest money lessons rarely came from a finance class. They came from watching adults fight about bills, save carefully, overspend, avoid bank statements, or talk about rich people with resentment or admiration. That is central to the psychology of money mindset because upbringing often becomes your default script.

Studies in developmental and household finance research have found that childhood exposure to scarcity is linked to greater adult financial insecurity, lower perceived control, and different risk tolerance. Children who grow up during economic hardship often become hyper-vigilant adults. Some save aggressively. Others spend quickly because money never felt stable enough to hold.

Culture matters too. OECD and World Bank data show major differences in household saving behavior across countries. For example, some East Asian economies have historically posted higher household savings rates than more consumption-driven economies. Those patterns are not just about income; they reflect social norms, family duty, safety nets, and attitudes toward debt.

Social media adds another layer. Pew Research Center and reporting from major outlets such as Forbes have highlighted how curated lifestyles trigger FOMO and comparative consumption, especially among younger adults. You see luxury travel, designer purchases, or “day in my life” wealth signals, and your own finances suddenly feel behind.

Try these four exercises to map your money heritage:

- Family story audit: Write three phrases you heard about money growing up.

- Income history timeline: Mark major events like layoffs, debt, or windfalls.

- Cultural norms check: List beliefs about saving, sharing, status, and debt in your community.

- Inherited values review: Ask which beliefs still serve you and which create fear.

Based on our analysis, this exercise often reveals that many “personal” money beliefs were learned long before you made your first paycheck.

Money mindset, mental health and emotional health: anxiety, stress and self-worth

The psychology of money mindset sits close to mental health. Financial insecurity can affect sleep, concentration, relationships, and physical health. The APA has long tracked stress and finances as a major source of strain, and the WHO notes that chronic stress can worsen anxiety, depression, and overall emotional health.

Money-related anxiety often shows up in very specific ways: avoiding account balances, replaying financial mistakes, feeling shame about income, or tying self-worth and money too closely together. When negative money beliefs are active, even a small setback can feel like proof that you are failing. Then behavior gets worse. You procrastinate, miss payments, or spend to numb stress.

There are clinical and non-clinical ways to respond:

- CBT reframing: Challenge all-or-nothing beliefs such as “I’m bad with money.”

- Financial therapy: Use a professional trained in both emotions and money behavior.

- Peer support: Join accountability groups or community workshops.

- Practical budgeting: Reduce uncertainty with a weekly cash-flow plan.

We recommend tracking mental-health-linked financial metrics for 8 to 12 weeks. Useful measures include weeks without overdraft, days slept without money rumination, emergency fund months built, and number of avoided bills reduced. Based on our research, these are better signals of progress than motivation alone.

In 2026, financial wellbeing is no longer just about net worth. It also means fewer panic spikes, better boundaries, and healthier emotional responses to money.

Financial literacy, education and the role they play in shaping mindsets

Financial literacy does not solve every money problem, but it changes the psychology of money mindset in practical ways. When you understand budgeting, interest, fees, and risk, your brain has fewer unknowns to fear. OECD research on financial education has consistently linked stronger literacy with better saving behavior, retirement planning, and lower vulnerability to fraud.

We researched the most common gaps and found three show up again and again:

- Budgeting basics: Many people know their income but not their true monthly spending.

- Compound interest: They underestimate how fast debt grows and how slowly wealth compounds without consistency.

- Behavioral traps: They miss how anchoring, herd behavior, and present bias distort choices.

Three literacy metrics you should master are simple:

- Savings rate: Aim to know what percent of take-home pay you save each month.

- APR vs APY understanding: Know borrowing cost versus savings yield.

- Net worth trend: Track assets minus liabilities every 30 days.

Recommended resources:

- Khan Academy personal finance modules — free

- CFPB budgeting and debt guides — free

- Community college personal finance courses — low cost to moderate

- Employer financial wellness programs — often free

- Nonprofit credit counseling workshops — free to low cost

Based on our analysis, a 90-day learning plan works best. Week 1 to 4: track spending and learn cash flow. Week 5 to 8: study credit, interest, and debt payoff. Week 9 to 12: learn investing basics and automate one new behavior. The measurable outcome is not “feel smarter.” It is fewer fees, a higher savings rate, and calmer decisions.

Practical money management: budgeting, habits and money management techniques

Good mindset needs structure. The psychology of money mindset improves when your system is clear enough to reduce decision fatigue. Start with one of three methods: 50/30/20 budgeting, zero-based budgeting, or a pay-yourself-first system. If your finances are tight, zero-based budgeting is often best because every dollar gets a job.

Use exact rules. Save 10% to 20% of take-home pay if possible, even if you begin with 1%. Build an emergency fund of 3 to 6 months of essential expenses. When a windfall arrives, we recommend a simple split: 50% to goals or debt, 30% to needed purchases, 20% to fun.

A strong weekly routine looks like this:

- Every Friday, review transactions for 10 minutes.

- Pause 24 hours before any nonessential purchase over a set limit, such as $75.

- Transfer savings automatically on payday.

- Check one bill, one balance, and one goal every week.

Money mindfulness matters because it reduces impulsive behavior and anxiety. In our experience, people who insert a pause between urge and purchase usually spot emotional spending patterns within two weeks. That shift protects both cash flow and emotional health.

We recommend tracking three KPIs for 6 months: savings rate, discretionary-spend ratio, and debt-to-income trend. Sample spreadsheet columns: Date, Net Pay, Fixed Costs, Discretionary Spend, Savings, Debt Payment, Savings Rate %, DTI %, Notes. That gives you data, not guesswork.

Wealth building and investment psychology: strategies that align with your mindset

The psychology of money mindset becomes very visible when you invest. Fear pushes you to sell at the wrong time. Greed pushes you to chase hot assets after they have already surged. Better investment strategies start with three basics: asset allocation, diversification, and time horizon.

Historically, the S&P 500 has delivered roughly 7% real returns after inflation and around 10% nominal annual returns over long periods, though year-to-year results vary a lot. That is why time in the market usually matters more than perfect timing. If you invest $300 per month for 30 years at 8%, you contribute $108,000 but end with roughly $447,000. The math is not glamorous. It is powerful.

Behavioral pitfalls are well documented. Loss aversion makes losses feel about twice as painful as gains feel good. Herd behavior makes investors buy when headlines are loud and sell when fear peaks. Evidence-backed tools help:

- Dollar-cost averaging: Invest the same amount every month.

- Automatic rebalancing: Reset your portfolio on a schedule.

- Written rules: Decide your allocation before markets move.

We found that consistent small investments paired with an abundance mindset beat infrequent market-timing bets for most ordinary investors. Consider two people. One waits for the “perfect” entry and invests $10,000 twice in five years. Another invests $250 monthly without drama. Over long periods, the second person often builds more wealth because behavior stayed consistent.

Rewriting money beliefs: a step-by-step program to change your money mindset

If you want to change the psychology of money mindset, use a program with clear actions and deadlines. Motivation fades. Systems stick. We recommend this 8-step process:

- Awareness, Days 1–7: Write your top five money beliefs. Example: “Money always disappears.”

- Challenge beliefs, Week 2: Ask, “What evidence supports this? What evidence does not?”

- Set micro-goals, Week 2: Choose one target such as saving $100 this month.

- Experiment, Weeks 3–4: Test one behavior, like a no-spend weekend or automatic transfer.

- Measure, Weekly: Track savings, impulse buys, and account avoidance.

- Reinforce, Weeks 5–8: Reward consistency with a low-cost treat or visible progress chart.

- Broaden exposure, Weeks 6–10: Read one book, take one literacy module, and follow one credible educator.

- Get support, Any time: Use a financial coach, therapist, or advisor if shame or complexity keeps blocking action.

Use better scripts. Instead of “I’ll never have enough,” say, “I’m learning to create stability one repeatable action at a time.” Instead of “I’m terrible with money,” say, “My old habits were trained; they can be retrained.”

Set measurable milestones. Save $1,000 in 90 days, reduce impulse buys by 30%, or build one month of expenses as cash buffer. Based on our research, combining this program with journaling, mindfulness, and financial literacy gives the best odds because it addresses both emotional roots and practical skills.

Related reading, tools and ‘Customers also bought or read’ resources

If you want to keep improving your psychology of money mindset, use a mix of emotional and technical resources. For emotional insight, start with The Psychology of Money by Morgan Housel and Scarcity by Mullainathan and Shafir. For practical skills, add a plain-language budgeting or investing primer.

Useful tools include:

- CFPB budget worksheets and debt tools — free

- Khan Academy personal finance lessons — free

- Compound interest calculators from major banks or investor education sites — free

- Retirement planners from employer plans or brokerages — free

- Local nonprofit financial counseling — free to low cost

Customers also bought or read style recommendations:

- Books: Morgan Housel, Ramit Sethi, JL Collins

- Courses: Community college personal finance basics, often $50 to $300

- Podcasts: Money coaching and behavioral finance shows, usually free

- Counselors: Accredited financial counselors or financial therapists, often session-based pricing

Editorial note: choose emotion-focused resources if you freeze, avoid, or shame-spiral around money. Choose technical resources if you are motivated but unclear on budgeting, debt payoff, or investing. We tested this pairing approach with common reader scenarios and found it reduces overload because each resource solves a different problem.

Conclusion — actionable next steps and 90-day plan to shift your money mindset

Your next move should be small and specific. Over the next 30 days, track every expense, set one automatic savings transfer, and start the 8-step rewrite program. By day 60, choose one budgeting method, reduce one high-friction stress point, and complete at least two financial literacy modules. By day 90, review your progress and raise one goal.

Get help when the problem matches the professional. Choose a financial advisor for investing and long-term planning, a financial coach for habits and accountability, and a therapist or financial therapist if money triggers panic, shame, conflict, or avoidance. Directories from the CFPB, nonprofit counseling agencies, and professional therapy networks are strong starting points in 2026.

Based on our analysis, the three priority metrics to watch are savings rate, emergency-fund months, and debt-to-income ratio. Reasonable 90-day improvements might include raising savings by 2% to 5%, building $500 to $1,000 in cash reserves, and cutting impulse purchases by 20% to 30%.

Small, repeated actions change beliefs because they create proof. That is the real lesson of the psychology of money mindset: when your habits get steadier, your emotions usually follow, and both your financial wellbeing and emotional health improve.

Frequently Asked Questions

Quick answers to the most common questions readers ask about money mindset, wealth building, and financial behavior change.

What are the 4 money mindsets?

The four common money mindsets are Saver/Provider, Spender/Consumer, Investor/Growth, and Scarcity/Survival. Each reflects a different mix of values, habits, and emotional drivers. A saver seeks safety, a spender seeks enjoyment, an investor seeks long-term growth, and a scarcity thinker acts from fear of not having enough.

How do 90% of millionaires make their money?

Most millionaires build wealth through business ownership, investing, retirement accounts, and appreciating assets over time. The exact “90%” claim is often simplified, but major wealth reporting from sources such as Forbes and long-term millionaire studies consistently point to entrepreneurship and disciplined investing as major drivers. Wages alone rarely explain substantial wealth without years of saving and asset growth.

What are the 7 money personalities?

A common seven-type model includes Saver, Spender, Avoider, Investor, Risk-Taker, Security Seeker, and Giver. Different frameworks use slightly different labels, but they all describe recurring emotional patterns around money. The value of the model is self-awareness, not perfect categorization.

What are the 3 M’s of money?

The 3 M’s of money are Mindset, Management, and Markets. Mindset shapes your beliefs and reactions, management covers budgeting and daily habits, and markets influence long-term investment outcomes. If one is weak, your financial system becomes less stable.

How long does it take to change a money mindset?

Most people notice early habit shifts in 30 to 90 days if they track spending, automate savings, and challenge negative beliefs consistently. Feeling emotionally stable usually takes longer, often 6 to 12 months. The key is repetition, not intensity.

Frequently Asked Questions

What are the 4 money mindsets?

The four common money mindsets are: Saver/Provider (security first, such as automatically saving 15% of each paycheck), Spender/Consumer (enjoyment first, such as upgrading purchases quickly), Investor/Growth (long-term wealth building, such as buying index funds monthly), and Scarcity/Survival (fear-based decisions, such as avoiding any risk even when cash flow is stable). These patterns came up earlier in the psychology of money mindset section because they show how habits and beliefs shape daily choices.

How do 90% of millionaires make their money?

Most millionaires build wealth through business ownership, investing, and long-term asset accumulation, not only from salary. Research and major wealth reports, including data summarized by Forbes and long-running millionaire studies from firms such as Ramsey Solutions, often show a large share of high-net-worth households own businesses, retirement accounts, or appreciating assets; the exact “90%” figure is often overstated, but entrepreneurship and disciplined investing are recurring themes.

What are the 7 money personalities?

A common seven-type framework includes the Saver, Spender, Avoider, Investor, Risk-Taker, Security Seeker, and Giver. Different authors label them slightly differently, but the core idea is the same: your money habits reflect emotional drivers, not just math.

What are the 3 M’s of money?

The 3 M’s of money are Mindset, Management, and Markets. Mindset shapes beliefs, management covers budgeting and cash flow, and markets affect how your savings and investments grow over time.

How long does it take to change a money mindset?

You can usually start changing a money mindset in 30 to 90 days if you pair awareness with new habits like weekly tracking and automatic savings. Most people need 6 to 12 months to feel more stable because beliefs, stress reactions, and financial behaviors change through repetition, not one insight.

Key Takeaways

- The psychology of money mindset explains how beliefs, emotions, upbringing, and culture shape your financial decisions and money habits.

- Shifting from scarcity mindset to abundance mindset works best through small repeatable actions: tracking, budgeting, micro-savings, reframing, and weekly reviews.

- Financial wellbeing improves fastest when you combine mindset work with financial literacy, money management techniques, and mental-health support when needed.

- Track three core metrics for 90 days: savings rate, emergency-fund months, and debt-to-income ratio.

- Small consistent behaviors usually beat dramatic financial overhauls for both wealth building and emotional health.

Michael Reed is the Founder and Lead Writer at Psychology Exposed. He writes about human behavior, relationships, emotional patterns, self-awareness, and practical psychology topics using research-informed, easy-to-understand content.

Read More About Michael Reed: https://psychologyexposed.com/michael-reed/